TipRanks

Billionaire Steven Cohen Building these 3 “strong buy” stocks

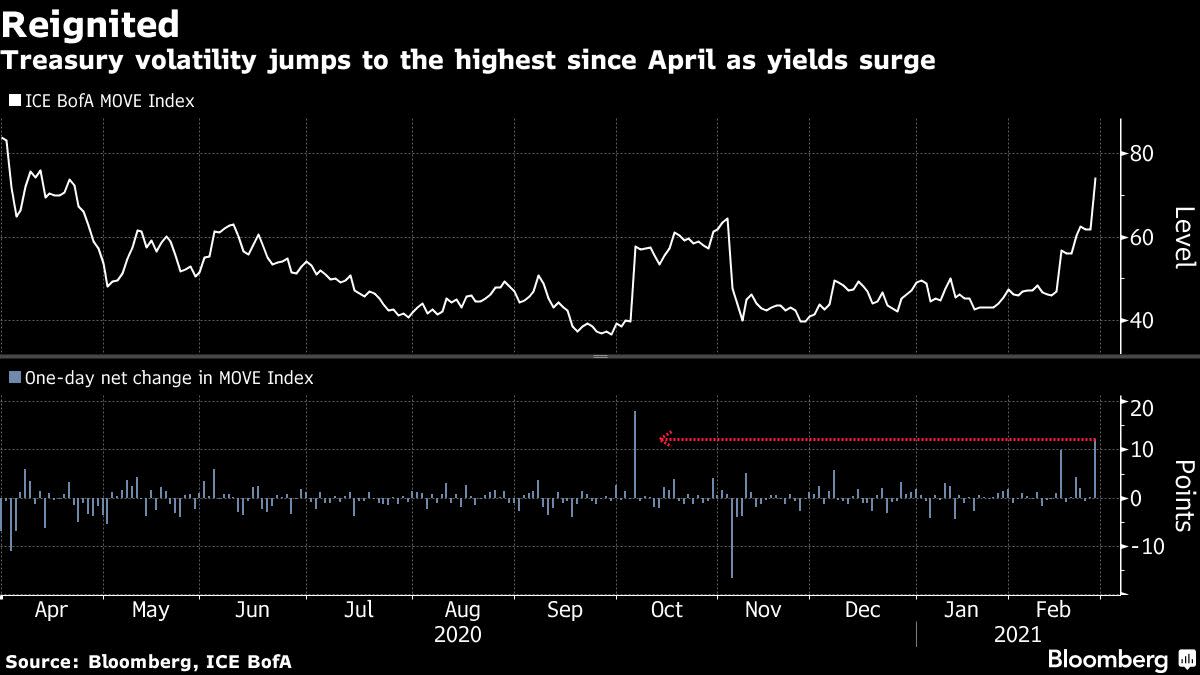

Last week, the NASDAQ slipped below 13,200, making the net loss from its full-time peak, which reached earlier this month, 6.4%. If this trend continues, the index enters a correction area, a loss of 10% from the maximum. So what exactly is going on? At the bottom, there are mixed signals. The COVID-19 pandemic is starting to decline and the economy is starting to reopen – strong things that should boost markets. But an economic resumption brings with it inflationary pressures: more people working means more customers with pocket money, and the big stimulus bills that have passed in recent months – and the a bill now working through Congress, which brings in $ 1.9 trillion – on extra money to put people’s wallets and liquidity into the economy. There is pent-up demand, and people with money to spend, and both factors will work to raise prices. We see one effect of all this in the bond market, where the ten-year Financial Link is up 1.4%, almost a year high, and has been going up from a few weeks ago. This could be a case of gunshot, however, as Federal Reserve Chairman Jerome Powell has said in evidence before the Senate that he is not considering a move to flat rates. encourage. In other words, these are difficult times. For those who feel lost in all the fog of the stock market, investment gurus can offer a sense of clarity. No one is bigger than the billionaire Steven Cohen. Cohen’s investment firm, Point72 Asset Management, relies on a strategy that incorporates investments in the stock market as well as a more macro approach. This strategy has solidified Cohen’s status as a highly-respected investment powerhouse, with the guru earning $ 1.4 billion in 2020 thanks to a 16% gain in Point72’s major hedge fund. With this in mind, our focus shifted to the latest 13F filter at Point72, which reflects the stocks the fund picked up in the fourth quarter. Locking in three tickets in particular, the TipRanks database revealed that each has won a “Strong Buy” analyst consensus and has great upside potential. Array Technologies (ARRY) Array Technologies is the first new position in a ‘tech company’ that provides tracking technology for large-scale solar energy projects. It is not enough to just use photovoltaic solar collector panels to power an energy facility; the panels must monitor the sun across the sky, and account for seasonal differences in their direction. Array delivers solutions to these problems with its DuraTrack and SmarTrack products. Array boasts that its tracking systems will improve the life efficiency of solar supply projects, and that its SmarTrack system can boost energy production by 5% overall. It is clear that the company has made a significant impact on the customers, as they have bases in 30 countries, in more than 900 convenience scale projects. President Biden is expected to take action to promote green economic policy at the expense of the fossil fuel industry, and Array could benefit from this political environment. The stock of this company is new to the markets, after holding the IPO in October last year. The event was hailed as the first major solar IPO in the U.S. for 2020, and was a success. Shares opened at $ 22, and closed the day at $ 36. The company sold 7 million shares, raising $ 154 million, and another 40.5 million shares were marketed by Oaktree Capital. Oaktree is the investment manager that has maintained a majority interest in the company since 2016. Array fans include Steven Cohen. Circulating up 531,589 shares in Q4, Point72’s new ARRY position is valued at more than $ 19.7 million at current valuation. Guggenheim analyst Shahriar Pourreza also seems optimistic about the company’s growth prospects, noting that the stock appears to be undervalued. “Renewable energy companies have seen a huge influx of capital as a result of the ‘blue wave’ and Democrat control of the White House and all chambers of Congress; however, ARRY continues to trade a significant discount for peers, “the 5-star analyst noted. Pourreza added,” We continue to be bullish on expectations ARRY’s growth is driven by 1) tracker market share advantages over fixed tilt systems, 2) ARRY market share advantages within the controller industry, 3) ARRY’s significant market opportunity in the less deep international market, 4) the opportunity to make money from their existing customer base over the long term through extended warranties, software upgrades, etc., which are very marginal. accretive. ”According to these bullish views, ARRY has Pourreza rates in the Buy segment, and its price target of $ 59 means 59% upside down from normal levels. (To check out Pourreza ‘s history, click here) New stocks in growth industries tend to draw attention from the benefits of Wall Street, and Array has recorded 8 reviews since it went public. Of these, 6 are Buyers and 2 are Holds, making the consensus level on the stock a Strong Buy. The average price target, at $ 53.75, suggests a place for ~ 45% upside in the next 12 months. (See ARRY stock analysis on TipRanks) Paya Holdings (PAYA) The second Cohen option we are looking at is Paya Holdings, a North American payment processing service. The company offers unified payment solutions for B2B jobs in the education, government, healthcare, nonprofit and convenience sectors. Paya boasts more than $ 30 billion in payments processed each year, for more than 100,000 customers. In mid-October last year, Paya completed its transition to the public market through the merger of SPAC (a specialist construction company) with FinTech Acquisition Corporation III. Cohen stands square with the bulls on this one. During Q4, Point72 raised 3,288,843 shares, bringing the holding size to 4,489,443 shares. After this 365% increase, the value of the position is now ~ $ 54 million. Mark Palmer, a 5-star analyst with BTIG, is pleased with Paya’s prospects into the mid-term, writing, “We expect PAYA to generate income growth in the teens high in the next few years, with Integrated Solutions ready to grow in the mid-20s and Payment Services set to grow in the mid-single figures. At the same time, the company’s operating costs should grow in the context of 5%, in our view. Therefore, we anticipate that PAITA’s growth will have changed EBITDA north to 20% in the next few years, and that the EBITDA adjusted margins will expand to 28% by YE21 from 25% in 2019. ” Palmer sets an $ 18 price target on PAYA shares, expressing his confidence in 49% growth for the coming year, and rating the shares as Buy. (To view Palmer ‘s history, click here) PAYA’ s Strong Buy analyst consensus level is unanimous, based on 4 Buy side reviews set a few weeks ago. The shares have an average price target of $ 16, which suggests ~ 33% upside from the current share price of $ 12.06. (See PAYA stock analysis on TipRanks) Dicerna Pharma (DRNA) Last but not least is Dicerna Pharma, a clinical-grade biotechnology company with a focus on discovery, research and development of treatments based on the RNA interventional technology platform (RNAi) aige. The company has 4 drug candidates in various phases of clinical trials and a further 6 in preclinical studies. The company ‘s pipeline has clearly caught the attention of Steven Cohen – eager to take a new share of 2.366 million shares. This tenancy is valued at $ 63.8 million at normal values. The most remote drug candidate is the Dicerna nedosiran pipeline (DCR-PHXC), which is being studied as a treatment for PH, or primary hyperoxaluria – a group of several genetic disorders that cause dys- life-threatening renal failure through excessive production of oxalate. Nedosiran inhibits the enzyme that causes this overproduction, and is in a Phase 3 test. High-end results are expected in mid-21 and, if all goes well. expected, NDA filing for nedosiran is expected near the end of 3Q21. Covering the stock for Leerink, analyst Mani Foroohar sees nedosiran as the key to the company’s future. “We expect to see an agreement nedosiran in mid-2022, putting the drug around a year and a half behind rival Oxlumo (ALNY, BP) in PH1 … A successful outcome transforms DRNA to being a commercially rare disease company in an attractive market duopoly with the best-in-class label, “Foroohar noted. To this end, Foroohar evaluates DRNA the Outperform (ie Buy), and has its price target of $ 45 suggests an upside capacity of 66%. (To check out Foroohar’s chart, click here) In total, Dicerna Pharma has 4 Buy reviews on the chart, making the Strong Buy DRNA shares are trading for $ 26.98, and their average price target of $ 38 is set at ~ 41% over the next 12 months. (See DRNA stock analysis on TipRanks ) To find great ideas for stock trading at attractive valuations, visit TipRa Best Stocks nks, a recently launched tool that unifies all TipRanks fairness views. Disclaimer: The views expressed in this article are those of analysts and are intended to use ntent for informational purposes only. It is very important to do your own analysis before making any investment.