It has been a difficult year for Intel and its shareholders. Negative business developments on the one hand (delay in launching advanced generations of processors) and on the other hand positive developments among the major competitors NVIDIA and AMD (continued dominance in GPU processors and ARM acquisition, at first and market share taken by Intel by AMD as well as announcement of XILINX acquisition) Powerful in the share returns of these three companies during 2020:

| The company | The stock’s return in 2020 |

| Intel | (19.9%) |

| Anvidia | 119.2% |

| AMD | 85.4% |

If you want to specialize in the capital market and have a big head and motivation, you can suit us.

The job can be part-time; Flexibility in working hours; Work from home too

Priority (optional) for writing experience and basic knowledge of the capital market.

Leave details and we will get back to you

Thank you for leaving details, we will try to get back to you soon

The level of future multipliers at which the shares of these companies are traded also indicates significant differences in the way investors estimate the future of these three companies. While the expectations in the case of Anvidia and AMD are for continued growth at high rates, to establish a dominant position each in its own field and to take market share from Intel, for Intel estimates are that the company is now at a crossroads and it is just time to make very important decisions.

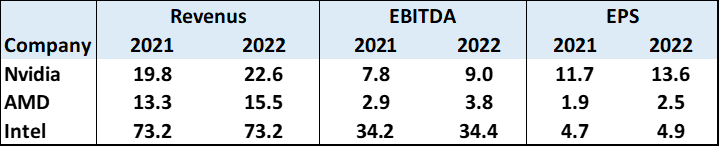

It is also worth noting the differences in the financial forecasts of the three companies. The table below shows the revenue forecasts, EBITDA (Earnings Before Interest, Tax, Depreciation and Amortization) and earnings per share of the three companies and estimates the performance differences between the companies.

It can be seen, for example, that Intel’s revenues for the next two years are about 6 times higher than those of AMD and more than 3 times higher than Anvidia. Intel’s projected profitability rates are also significantly higher than those of its competitors. Just to put things in proportion, Intel’s EBITDA exceeds three times all of AMD’s revenue in the fourth quarter of 2020.

And yet, as also reflected in the behavior of stock prices, and the market value of the three companies, Intel is in a not-so-simple business situation and the investing public believes more in the growth and dominance prospects of Anvidia and AMD and less in those of the CPU queen and Moore Law inventor.

“2020, I will die” – Intel version

I will briefly review the main events. During the first quarter of last year, AMD continued the trend of the past two years in which it managed to take market share from Intel in the X86 PC processors market. The change is the result of a number of significant changes in this market that have taken place in recent years. These changes include the undermining of the wintel alliance between Intel and Microsoft, the transfer of production of AMD’s processors to TSMC and, as a result, the improvement in AMD’s profitability, the narrowing of the technology gap between companies’ processors that reduced AMD’s market share in Intel. Prices.

The following graph shows the increase in AMD’s market share compared to the decrease in Intel’s in the field of PC processors in the last 8 years. The gap has narrowed especially in the last two years when in the third quarter it stood at only 62:38 in favor of Intel,

Source: statista.com

Then came the second quarter. Despite not bad results and success in bypassing business forecasts, the company’s management issued a dramatic announcement that production of 7 nm processors will be delayed by six months compared to the original forecast, ie for the first half of 2023. With this in mind, AMD manages to take market share from Intel Manufactured by TSMC at a resolution of 7 nm, investors’ concern is reflected in a 16% drop in the share price, the day after (24.7.2020). The impression created is that the technological gap in manufacturing between Intel and TSMC is deepening. On the one hand, Intel, which is expected to move to create a resolution of 7 nm only during 2023, compared to TSMC, which already produces 7 nm and also more advanced resolutions of 5 and even 3 nm …

The results in the third quarter also disappointed. Intel barely managed to reach the (low) forecast it gave, but failed in one of the important parameters – revenue of the data centers division – which fell by 7% compared to the forecast, and feared market share losses to major competitor Anvidia.

Other events that negatively impacted the stock price during 2020 were Apple’s announcement of the process of manufacturing processors for Macs from Intel to create its own, Amazon moving to self-create processors for its cloud computing activity, as well as Microsoft and Google.

Exchange of CEOs at Intel

After a flood of unfavorable business developments, Intel announced a change of CEO in mid-January 2021, with Pat Glazinger, CEO of VMWare and former head of Intel’s Chief Development Officer and employee of the company for about 30 years, taking on the challenging role. The announcement made Intel’s shareholders very happy and caused a 12% jump in the share price (and a 5% drop in the VMWare share price, which may indicate that it is a significant replacement). Unlike the current CEO, Bob Swan, Gelsinger is an engineer, in the best of the ‘intellectual’ tradition, and the hopes of the shareholders are high.

Intel faces strategic challenges that will take a long time to realize. The biggest and most significant challenge is whether to continue manufacturing activity, within the company, or to direct this activity to external parties as Anvidia and AMD do with TSMC. The answer to this question is complex and part of it has already been given in the investor talk of the fourth quarter results of 2020, published on 22.1.2021. The incoming CEO said he was pleased with the progress made in developing the 7-nanometer processors and that he believes most of the production of the various products during 2023 (the launch year of the 7-nanometer program) will be done within Intel. However, he estimates that Intel will increase production through external manufacturers Compared to what it is today, Intel manufactures about 15% -20% of products that are not processed by external manufacturers, the majority by TSMC and it will start producing through TSMC processors for personal computers, with advanced technologies of 5 and 3 nm starting from the second half of the year.

Despite the good business results achieved by Intel this quarter, which also included raising the forecast for the coming quarter, the stock recorded a 10% decline as investors hoped to hear the new CEO make a significant U-turn and move the company to a model of outsourcing manufacturing activity.

However, keep in mind that the new CEO will only take up his post and will likely submit a more detailed and significant strategic plan in the coming months. I estimate that even if it is decided to outsource a significant portion of Intel’s production, implementing such a plan and impacting business results (The good ones, it must be said) will take a long time.

What do the analysts think?

The Intel stock is covered by 44 analysts from the sell side, a huge amount by all accounts. As can be seen in the following table, there is an unsurprising correlation between the events that have taken place in the shares of Anvidia, AMD and Intel in the past year. 38% of analysts surveying Intel are on a buy recommendation, compared to 78% and 55% for Anvidia and AMD respectively.

| No. of analysts | buy | neutral | sale | Target price average | % Of target price | |

| Intel | 44 | 17 | 17 | 10 | $ 64 | 12% |

| Anvidia | 41 | 32 | 6 | 3 | $ 590 | 10% |

| AMD | 40 | 22 | 14 | 4 | $ 100 | 15% |

Such things take time

Intel is today at a strategic crossroads and is required to make crucial decisions that will affect its future in the coming years. It’s too early to talk about the probability of success, but it seems that the new CEO has promising opening figures and more details we will know after announcing in the coming months his strategic plan for Intel’s success and return to growth. Intel faces high competition from Anvidia and AMD when both These companies made two huge acquisitions in the fourth quarter of 2020 (Anvidia acquired ARM and AMD acquired Xilinx), thus strengthening their position vis-à-vis Intel in the areas of cloud, AI and 5G infrastructure. There is also a threat from technology giants (Amazon, Microsoft and Google) to produce the processors For their cloud operations from home and not through Intel and also Apple will stop being an Intel customer in its new processors.

It seems that 2021 is going to be an interesting year …

Rami Rosen, senior analyst and investor relations expert.

The information presented in this review constitutes general information regarding the activity of the company under review and is only auxiliary material and should not be regarded as factual or complete and exhaustive information of all aspects involved in investing in securities, The above does not constitute investment advice / marketing and / or a substitute for investment advice / marketing and / or tax advice by those who are authorized to do so, who take into account the data and the special needs of each person.