State ICs & Total PUA

Universal Value Advisors

The year finally came to an end, and, as usual, the latest data continued to decline.

Despite the weak economic data, the equity market closed this year at high-term levels. The S&P 500, at 3,576, rose 10.5% for the year after falling 34% in February / March, well back.

It is a market mantra right now, with the vaccines now distributed, and despite issues there, before spring / summer consumers feel confident enough to return to some pre – consumption habits. and economic growth in the second half of 2021 will be “V” shaped. With the data, this looks like optimistic thinking.

As the New Year begins, major changes have already taken place in a process that will shape the appearance of the “New Normal” economically. Three such changes are: 1) rapid growth of businesses and wealthy people from high tax / high cost states; 2) the apparent demand for office space in major U.S. cities; and 3) major changes in the way Hollywood distributes its products.

The Economy

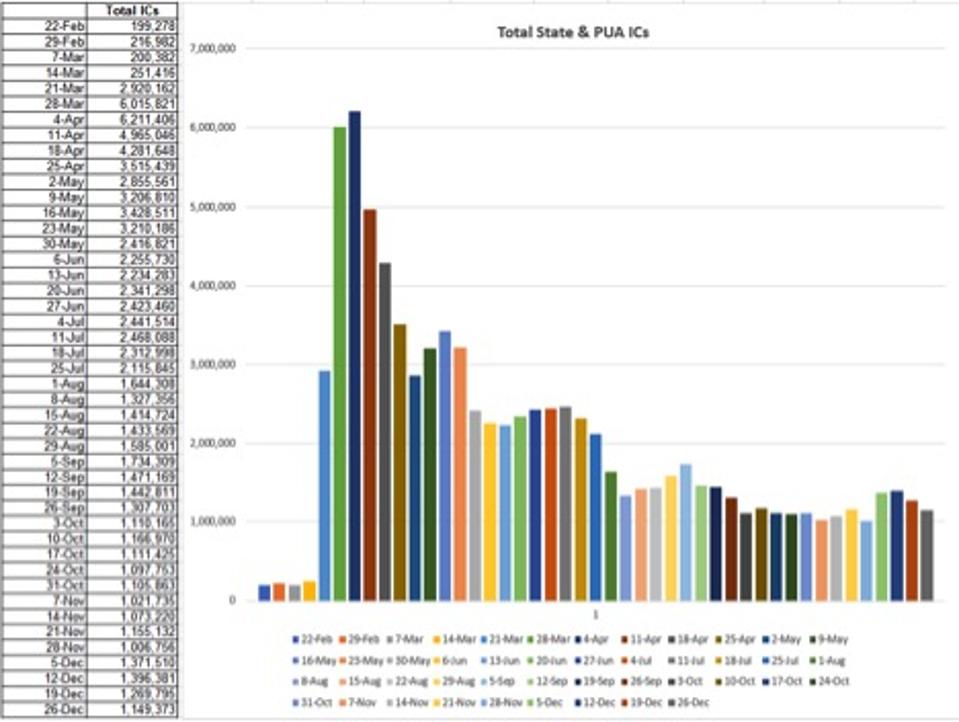

The week ended 26 Decemberth showed 1.15 million new unemployment claims, still high in the air. There was a -32K fall in state unemployment programs and a -88K drop in PUA (Pandemic Unemployment Assistance) programs. The fall in these numbers is, of course, due to holiday issues rather than any real improvement. The chart attached at the top of this blog shows that Initial Applications (ICs) are still well over 1 million / week. They are sure to get worse in January.

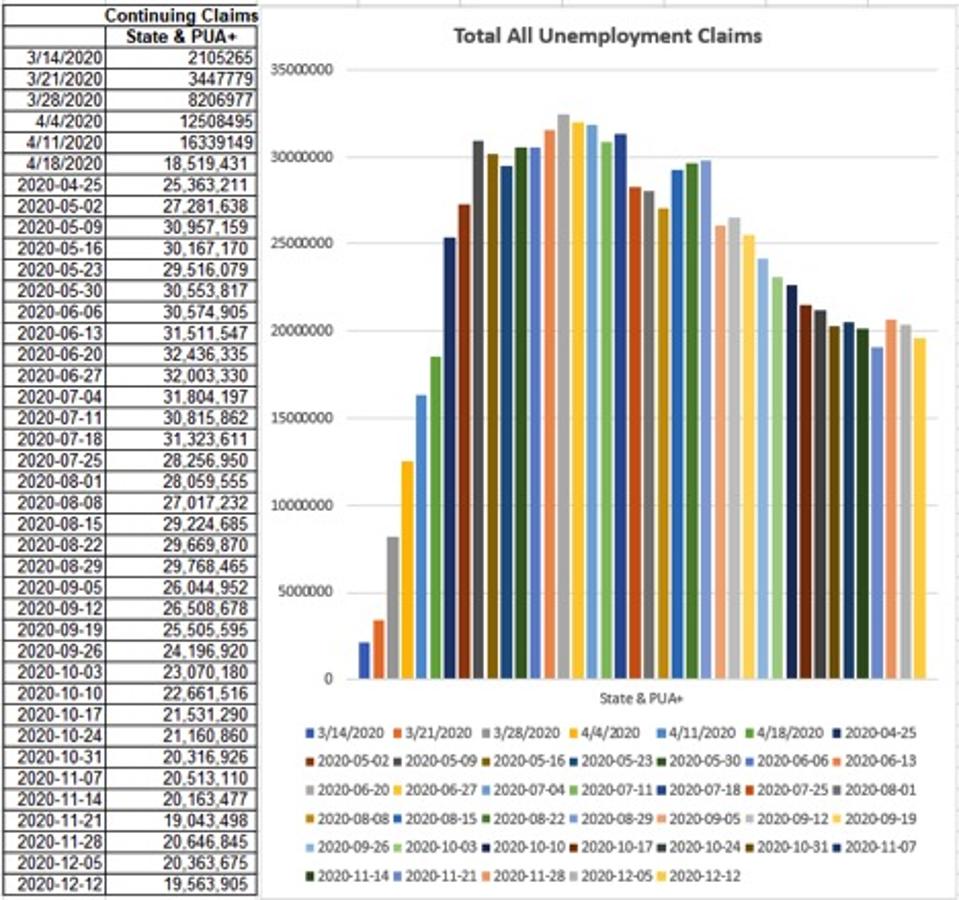

In addition, total state and Continuing PUA (CCA) applications still reach nearly 20 million (see chart and chart) as of mid-December. Think of this in terms of a workforce of about 165 million. That means an unemployment rate of more than 12%.

All unemployment claims

Universal Value Advisors

Other data:

- Upcoming home sales, a key indicator, fell -2.6% M / M in December;

- New home sales were down -11% M / M in November and down four months in a row;

- The University of Michigan Consumer Sentiment Study showed a sharp decline in home and auto purchase intentions;

- The latest NY Fed Credit Accessibility Survey reveals that a decline in consumer credit has begun, not just what is needed to stimulate growth in an economy whose GDP is a 70% consumption;

- The NY Fed found that 72% of survey executives said business conditions were lower than normal in December and that they did not expect any improvement for the next six months.

- The regional Fed services indexes are shown in the table below – find a pattern?

Regional Feeding Services Index

Universal Value Advisors

Financial Markets

As mentioned above, 2020 equity markets closed at the highest levels. History shows that market values are at nose levels. However, history also shows that almost all major market corrections are driven by the central bank. Given that the Fed has announced a “place of residence” by 2023, a major correction seems to be a low odds bet, and, although something in the 10% -15% range could happen, the Fed will definitely get involved before it goes too far. In fact, this Fed believes that the “wealth effect” of higher equity prices will “fall. “Because it has not done so over the last 14 years of easy money, and as income inequality is getting worse, it seems that it is not playing in the realm of Fed this.

Therefore, with the support of such Fed and the introduction of the vaccines to the general population, the normal market statement is that, in such a low environment, a return to “normal” corporate profits will return with “V-shaped growth ”In the second half of 2021. As soon as the virus goes down, pent-up demand will cause users to spend, spend, spend. So the “V.”

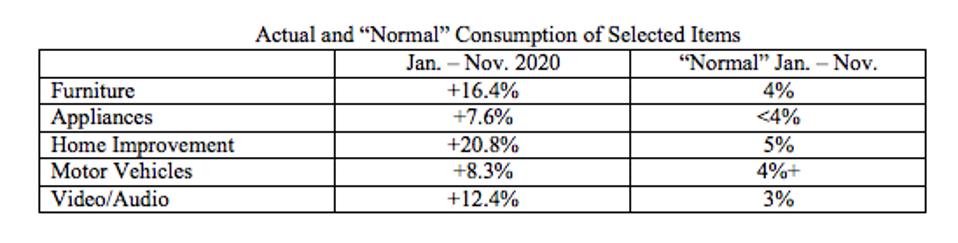

“V” does not stand for “Viable”

This idea is flawed because it has done so in general all wear was suppressed. The following table shows the January to November 2020 expenditure on semi-large and large consumer items and what would be expected in the January-November “normal” period:

Actual and “normal” use of selected materials

Universal Value Advisors

The shift from consuming services to consuming goods during the pandemic may have found great demand for such. As a result, in the upcoming scenario of “return to normalcy,” the growth rates of these important factors tend to be below their historical norms. Therefore, the “V” may be greater than “u. ”Clearly, this logic is not in today’s equity market.

The “New Normal” is starting to take shape

The length of the pandemic is now gaining momentum; tasks that will surely shape the “New Normal. “High taxes and high costs of living in some states seem to be forcing individuals and businesses to find more cash-strapped / business-friendly places, especially in an environment where work from home (WFH) ) able.

Everyone who reads this is probably aware that Tesla’s

TSLA

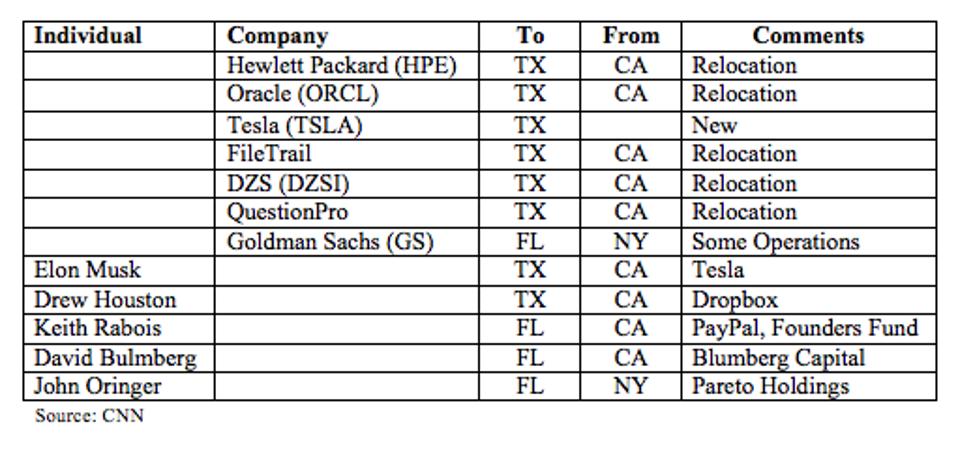

Transaction under companies (CNN Source)

Universal Value Advisors

The Austin, Texas Chamber of Commerce has a list of companies that moved there in 2020; 120 in total, creating 15,833 new jobs. Of the 120 companies, 24 were ready to hire 100 or more employees, of those 24, only six moved to Austin from within Texas. Of the other 18, 10 came from California and 4 from Washington state (one each came from GA, MI, India and the UK). Such an industry will move from high tax / high cost states to lower cost / lower tax states as a sign of the “New Normal” that 2021 will bring!

In the Real Estate Trading (CRE) market, companies are abandoning office space at an alarming rate. Christmas Eve Headline in the Financial Times read: “US Office Space Dumped Up After Success Working From Home,” (FT, 12 / 24,20, p. 7). The market will take years of office space to overcome, if ever. So too, with growing reliance on package delivery and internet shopping since the outbreak began, shopping malls will continue to struggle.

Another major difference in “normal” appearance occurs in film entertainment. All major theater chains are struggling to survive with revenues down -94% Y / Y. Pre-pandemic movie theaters enjoyed a 90-120-day ban with the latest Hollywood releases , especially the blockbusters. However, after several recent announcements, some major film studios have decided (at least in the future) to release new blockbusters at the same streaming media at the same time as they are released to the theaters. For instance, Wonder Woman 1984 first on HBO Max on Christmas day. Others have changed their policies to give theaters a much shorter ban period. It beats anyone as it shakes out. But one thing is certain; this will have a major impact on the film theater industry.

Conclusions

Markets are looking beyond the economic factors that are likely to grow due to smooth Q4 GDP growth and possibly negative growth (double-digit decline?) In Q1. Markets have assumed that the virus will lose and a “pent-up” demand will trigger a “V” recovery in the second half of 2021. The data shows that consumers have use of some items with large tickets in 2020, indicating that demand for such items could be in circulation for some time. This could have a very positive effect on the “V” shaped recovery position.

In addition, trends are now emerging that give us an idea of what the “New Normal” will look like as time goes on. One such move is the rapid depletion of businesses and a wealthy person from high tax / high cost states to more business friendly ones. At this point, exodus states do not appear to be taking steps to reverse that aspect. Other views on the “New Normal” can be seen in the headlines in terms of overcrowding and the entertainment industry distributing its products.

One thing is clear: “Normal” will not look like it did in February last year.