Brothers Shaul and Dori Naoi were pioneers in the field of non-bank financing, when in 2011 they registered the company

Naoi

+ 5.36%

Base:1,753

opening:1,753

High:1,864

low:1,760

change:2,054,432

Page Quote News Graphs Company Profile Recommendations

More articles on the subject:

Trading in the stock market by merging into a stock market skeleton. In the first years, the capital market loved Naoi. The company grew, profits increased and the stock rose accordingly. From 2013 to 2017, the company increased its loan portfolio, but the net profit remained at about NIS 60 million per year. The company’s explanation was the process of improving the customer portfolio, ie choosing better customers, who accordingly receive money at a cheaper price from the company. But this explanation is partial, the company changed its business focus in those years.

If you want to specialize in the capital market and have a big head and motivation, you can suit us.

The job can be part-time; Flexibility in working hours; Work from home too

Priority (optional) for writing experience and basic knowledge of the capital market.

Leave details and we will get back to you

Thank you for leaving details, we will try to get back to you soon

From focusing on discounting deferred checks from third parties, Naoi has moved to focus on discounting independent deferred checks (loans). As of the end of 2016, approximately 71% of the customer portfolio had discounted independent checks, and has remained at these levels ever since. In 2019, the company entered a new field of activity, the purchase of bonds on the stock exchange of companies with a similar risk profile to the company’s customers.

Exercise of the brothers’ shares and termination of the dividend distribution policy

After 5 years of fixing the company’s net profit, brothers Shaul and Dori reduced their share in the company to about 34% in 2017, after selling about 8.5% of the company’s shares, for NIS 68 million, at a price of NIS 25 per share. This sale has completed a series of realizations worth approximately NIS 220 million since 2013.

In addition, towards the end of 2017, the brothers canceled the company’s dividend policy, which was announced in 2014. The announcement of the cancellation of the dividend policy surprised the capital market and led to a 16% drop in the share, despite the company explaining that the cancellation of the dividend policy was intended to expand.

Another negative news that came out that year was that the manager of the Jerusalem branch, Avraham Hinitz, sold all his holdings in the company for about NIS 7 million, right after the announcement of the cancellation of the dividend policy.

Struggle over the reward model, Entropy’s opposition in 2019

Until the approval of the meeting in 2019, the salary cost of each of the brothers was NIS 1.2 million and a performance-based bonus of NIS 700,000 per year. The brothers wanted to fix the compensation package for each of them for NIS 3.4 million.

The institutional consulting firm, Entropy, opposed the renewal of Shaul Nawi’s appointment as chairman of the company, and also opposed a pay rise for Shaul Naoi’s daughter, Noy Naoi, the company’s legal counsel.

The one who decided the discussions was the Altshuler-Shaham investment house, which held about 25% of the company’s share capital. The compromise announced was that Shaul Naoi would resign from his position as chairman and be appointed co-CEO alongside Dori Naoi. The cost of the approved compensation package for each was NIS 2.9 million, instead of NIS 3.4 million. In addition, an employee was appointed chairman of the company and the remuneration of the daughter of Shaul, the company’s legal counsel, is not different.

The dramas of 2020

The year 2020 began with a report that Shaul Naui was investigated on suspicion of committing reporting offenses in the case of the suspected use of inside information by Ami Goldin, a former foreign lawyer at the company. In May 2020, Dori Naui surprised the capital market with an announcement that he intended to move to Miami in the US , And run the company from there. That same month, another, no less surprising announcement came out, in which Shaul Naoi revealed that he was retiring from the management of the company and selling his share to his brother Dori at a significant 25% discount on the market price. A few days later, Dori Nawi again surprised the capital market and announced that he had decided to stay in Israel.

Situation 2021 – Where does the company stand today?

who is the boss?

The controlling owner of the company is Dori Naoi, who holds about 39% of the company’s shares, after buying the share of his brother Shaul and other shares on the stock exchange. Another major holder is the Altshuler-Shaham investment house, which holds approximately 21% of the company’s shares through the provident and pension fund (15.55%), the mutual funds (5.88%) and the Altshuler-Owl hedge fund (0.09%). The rest of the shares, about 39% of the company’s capital, are held by the public.

The only company in the field that is traded below equity

Naoi is the only non-banking financing company, which is traded below its equity. The company is traded at a market value of NIS 560 million, while the company’s equity stood at NIS 586 million as of September 30, 2020. Equity is likely to increase with the publication of the company’s annual reports. The company maintains financial stability with an equity ratio of approximately 35% of the balance sheet.

The declining trend in the customer credit portfolio has stopped – will the trend change?

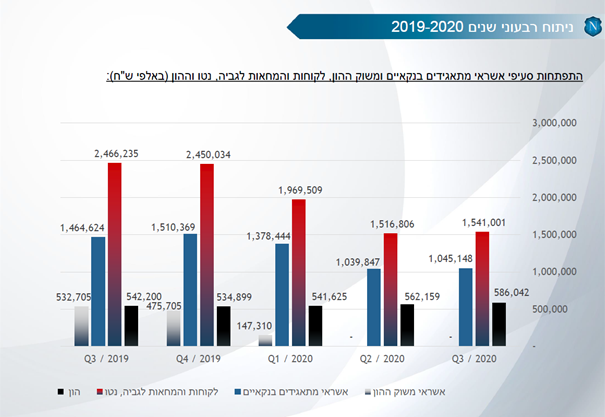

The company reduced its credit portfolio, from NIS 2.5 billion in the third quarter of 2019 to NIS 1.5 billion in the second quarter of 2020. During this period, the company repaid all credit from the capital market and currently funds its operations by bank credit and equity only. In the third quarter. Of 2020, the downward trend in the customer portfolio stopped, and we even saw a small increase of about 2%.

Source: The company’s presentation to the capital market – December 2020

The balance of the customers’ credit portfolio amounted to approximately NIS 1.54 billion on September 30, 2020, with the share of credit backed by deductibles (loan) amounting to approximately 74% of the total balance of the portfolio. Because of its business focus on stand-alone relays, Naoi “rolls over” its portfolio more slowly compared to competing companies. About 67% of all relays are repaid within a period of up to 180 days.

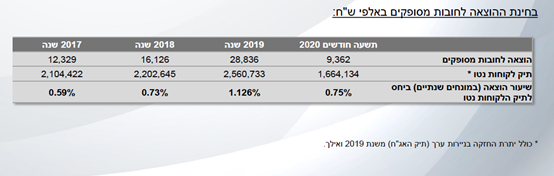

One of the most important data in credit card companies is the expense of doubtful debts in relation to the customer portfolio. The rate of doubtful expenses in the first 9 months of 2020 amounted to 0.75%, similar to 2018 and significantly lower than in 2019. In an interview with BizPortal in December, Dori Naoi said: “When our peace asks for a postponement he enters the watch list and is immediately set aside. Ours is higher than normal periods. ” It is likely that if the peak of the crisis is already behind us, we will see a decline in the rate of expenditure on doubtful debts.

Source: The company’s presentation to the capital market – December 2020

The most profitable company in the industry in the third quarter returned to dividend distribution

Naoi recorded a net profit of NIS 18.3 million in the third quarter of 2020, the highest quarterly profit in the non-bank financing industry. The data for the fourth quarter have not yet been released, but it can be assumed that the company will present a good fourth quarter, and in fact Naoi will trade at a single-digit profit multiplier below 8. So the question arises, did the capital market punish the sibling group too well?

After the cancellation of the dividend policy about 3 years ago, the company returned to distribute dividends in December of 2020. It will be interesting to see if the company will continue to distribute dividends in the coming years as well.

Source: The company’s presentation to the capital market – December 2020

Naoi Looking Forward – What Will Brother Naoi Do?

The company’s past is very important, but the price in the capital market is determined by the company’s future. In terms of price, Naoi stock is cheap relative to companies competing in the industry. In my opinion, at this point the company should get a lower multiplier because of: anemic growth in profitability, lower return on capital and of course the background dramas in recent years.

Dori Naoi is the sole owner of the company, with a respectable reward model, and now the ball is solely in his hands. I hope Dori’s goal is to bring value to all the shareholders in the company. If I could advise Dori and the company’s board of directors, I would suggest they improve transparency and better explain where the company is going. Of course one must stop with dramatic messages, which undermine trust.

One last thing I would recommend is to maintain corporate governance and respect the institutional ones. Family is important, and family businesses are often even more successful, but Naoi is a public company and should act accordingly. There is no doubt that according to the price on the stock exchange, the company has lost the confidence of the capital market. The good news is that it can be rebuilt by the right decisions of the company management for the benefit of all shareholders.

So back to the question we started with – did the capital market punish the company too much?

This is a question that every investor will have to answer for themselves.

Key risks:

1. Dori Naoi – a key man.

2. Economic situation in the economy – affects the non-bank credit market.

The ability to raise bank credit.

4. Altshuler-Shaham can sell shares in the market and put pressure on the share price.

Amit Shamir is the CEO of the Kepler Capital hedge fund.

Due Diligence: The above should not be construed as a recommendation to perform operations and / or investment advice and / or investment marketing and / or advice of any kind. The information presented is for information only and is not a substitute for advice that takes into account the data and the special needs of each person. Anyone who uses the above information – does so at his own discretion and sole responsibility. Kepler Capital and / or the author hold and / or may hold some of the papers mentioned above.

The publication of this information does not constitute an offer to the public to invest in a partnership. The investment in the partnership is on the basis of a private offer only, subject to the limitations as specified in the provisions of applicable law, and at the absolute and exclusive discretion of the general partner.