UKRAINE – 2021/02/15: This photo shows the Walmart logo displayed on a smartphone and … [+]

SOPA / LightRocket Images via Getty Images

Walmart (NYSE: WMT) expects to report its fourth-quarter fiscal results on Thursday, Feb. 18. We expect WMT to outperform revenue and employment expectations, on led by growth across all reporting sectors — Walmart US, Walmart International, and Sam’s Club. The big box retailer has benefited from its low prices and improved digital presence – all while benefiting from its vast network of brick-and-mortar stores. We expect the company to continue to outperform the market in the upcoming Q4 release, thanks to its leadership position and improving earnings outlook.

Our forecast reveals that Walmart’s valuation is $ 150 a share, which is 4% higher than the current market price of over $ 144. Take a look at our interactive dashboard analysis WMT Prerequisite: What to expect in Q4? for more information.

(1) Revenue is expected to be slightly ahead of consensus estimates

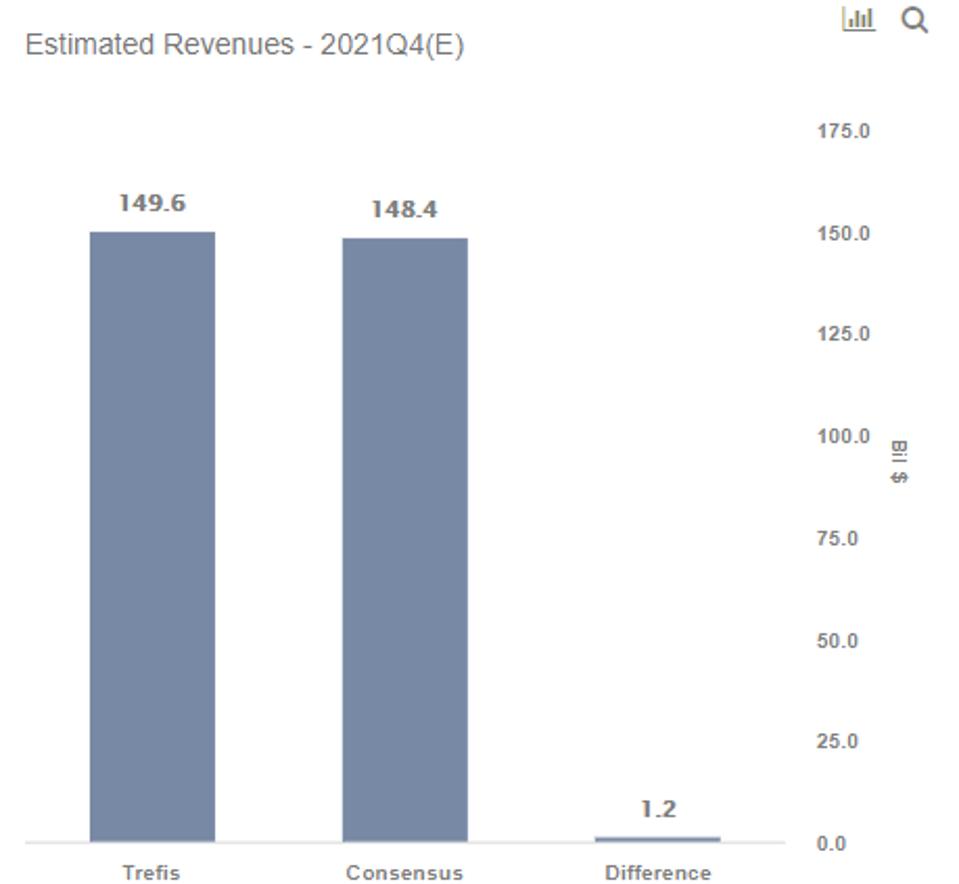

Trefis estimates that Walmart’s Q4 2021 revenue will be around $ 149.6 Bil, slightly ahead of the consensus estimate of $ 148.4 Bil. The Covid-19 crisis boosted sales of essential products at both Walmart and brick-and-mortar online stores. As a result, vendor revenues grew 6% year-over-year (yoy) to $ 407 billion in the first three quarters of fiscal 2021 (year to January 2021). The company showed its progress on this score by posting 10% higher relative asset sales in fiscal Q1, a 9.3% increase in Q2, and a 6.4% increase in Q3. In fact, the company’s push into digital enterprise seems to be working as nearly 90% of the increase in Q3 companies (which ended in October) came from e-commerce sales. We expect the company to continue cycling this growth trend in Q4 as well.

Walmart e-commerce sales skyrocketed through the pandemic, up 74% in Q1, 97% in Q2, and 79% in Q3 – making room for an attractive time to membership service launch e-commerce. The vendor has launched a new Walmart + loyalty program

WMT

2) EPS tends to be well ahead of consensus estimates

Q4 2021 WMT earnings per share are expected to be $ 1.59 per Trefis analysis, nearly 6% above the consensus estimate of $ 1.50. While the retailer has seen Covid’s costs rise so far this year due to special hourly employee bonuses, higher pay in performance centers, and an abstract increase in digital sales in the quarter, the growth helped stronger revenue by adjusting these costs.

For the full year, we expect Walmart’s net margin to grow slightly from 2.8% in fiscal 2020 to 2.9% in fiscal 2021. This could, along with 5% yoy growth in Walmart’s revenue , leading to an increase of $ 1 billion yoy in net. revenue to $ 15.9 billion in 2021. All of this, leading to a potential EPS increase from $ 5.22 in FY 2020 to around $ 5.56 in FY 2021.

(3) Measure stock price higher than normal market price

Going by our Walmart valuation, with an EPS estimate of around $ 5.56 and a multiple P / E of 27x in fiscal 2021, this translates to a price of $ 150, which is 4% higher than the market price currently of over $ 144.

While WMT stock looks attractive heading into its Q4 release, 2020 has created many price stops that will provide attractive trading opportunities. For example, you will wonder how the stock valuation for Starbucks vs Home Depot appears disconnected with their relative operational growth. You’ll find a lot of incoherent couples here.

See everything Trefis price estimate and Download Trefis Data here

What’s behind Trefis? See how it empowers new collaborations and what they are CFOs and Finance Teams | Product, R&D, and Marketing Teams